A couple of weeks ago I came across a really interesting article titled “How Leaders Succeed in an Era of Volatility” in

IndustryWeek by Mark Pearson of Accenture. Mark discusses how some US manufacturing companies have recovered more quickly than others by investing in talent and capacity. The interesting point he makes is that the companies that have recovered most quickly are those that invested in new capacity in areas with existing talent pools. Mark contrasts this with companies that have either increased or consolidated their capacity in areas of revenue growth. Mark states that

When they relocated, leaders and non-leaders alike were motivated by the reduction of operating costs (100% versus 87%). In opening new operations, leaders reported doing so not so much to reduce costs (47% to 61%), but to take advantage of unique skills in the new location (42% versus 10%). Non-leaders were more likely to say they opened a new facility to increase customer responsiveness (21% versus 39%).

Given the rapid increase in fuel costs this is somewhat counter intuitive. But, while lacking specifics, Mark concludes that

In an era of persistent volatility, the recovery leaders rose to the challenges. They focused on their business and investment objectives, made wise decisions in their physical networks and better maintained the appropriate resource/talent mix in their enterprises. As a result, today they find themselves aligned with a new business environment in a way that is allowing them to sprint more confidently into the future.

Reading this article sent me on a search of the web for articles that would support Mark’s point of view. There were many, including Deloitte’s 2012 Global Outsourcing and Insourcing Survey, which concludes that

- Current and future outsourcing: The outsourcing market continues to confuse outsourcing with offshoring. Many respondents still see the two processes as inseparable – even though many times outsourced work never leaves the originating country.

- Contract performance and relationship management: Vendor management organizations, while highly competent at day-to-day activities, find themselves underutilized when it comes to driving strategic value.

- Most recent outsourcing experience: Respondents list “underestimating scope by the vendor” as the largest contributor to deal dissatisfaction, and respondents use vendor communications and escalations most often to remedy deal dissatisfaction.

- Cloud sourcing: Though often discussed and promoted, there continues to be a substantial amount of uncertainty about cloud-based outsourcing and its future adoption.

There is a lot I could comment on in the Deloitte conclusions, but the one I want to focus on is the manner in which we use outsourcing and offshoring interchangeably, especially given that we are also seeing the same confusion between insourcing and onshoring. This confusion can be seen in an article in The Atlantic titled “The Insourcing Boom” of which the first paragraph is

After years of offshore production, General Electric is moving much of its far-flung appliance-manufacturing operations back home. It is not alone. An exploration of the startling, sustainable, just-getting-started return of industry to the United States.

Notice the confusion. I don’t know why The Atlantic didn’t refer to the phenomenon as onshoring, but they are not alone. Heck, even President Obama is confusing the terms using the term insourcing in his State of the Union address in 2012. Given the degree to which outsourcing has been coupled with offshoring this confusion is understandable. But the President he can be forgiven for the confusion because from his perspective onshoring – bringing jobs back to the US – is synonymous with insourcing, but not for companies. True insourcing is, for example, GM’s intent to insource 90% of IT jobs. But even here the lines are blurred despite the fact that the author’s point is that “GM’s plan to grow its own payroll instead of handing the work to subcontractors.” Of course many of the jobs outsourced to their subcontractors were then offshored by the subcontractors. That’s how they made their money. While I applaud every manufacturing job that is repatriated, whether in the US or elsewhere in the West, I find the discussion rather quixotic, which Dictionary.com defines as “extravagantly chivalrous or romantic; visionary, impractical, or impracticable.” Given that I have been in Barcelona the past week I couldn’t resist the reference to that ultimate example of a foolish quest by Don Quixote, who, according to Wikipedia, “…, dreams up a romantic ideal world which he believes to be real, and acts on this idealism, which most famously leads him into imaginary fights with windmills that he regards as giants.” There is no doubt that some manufacturing and IT jobs will return to the US, and the West in general, because the pendulum swung too far, raising issues of supply chain responsiveness and inflexibility, not to mention the difficulty of managing volatile transportation costs and fluctuating exchange rates. But I am firmly in the camp of George Stalk of Boston Consulting Group who wrote an article for the Harvard Business Review in June 2011 titled “What the West does not get about China”, in which he includes the diagram below.

The key point being that while from a labor perspective the discussion is correctly on offshoring versus onshoring, the real opportunity for the West is to develop products to satisfy the needs of the growing middle class in Asia, particularly China and India. While only in my wildest personal fantasy can I be equated with George Stalk, this is something I have been writing about for several years. (Recession or Reset?, An Imminent Threat to Western Brands, and The Shifting Sands of World Economies.) As Stalk writes,

The rise of local competitors will happen faster than most multinationals expect. MNCs (multi-national companies) that hope to have strong market share in China in a few years need to establish themselves now.

In June 20111 China already ranked first in consumer spending in five categories and second in another 5 categories. And already there are Asian brands in these categories that are bigger than Western brands and which are largely unknown in the West, Huawei and Haier as key examples. Interestingly Unilever has found that brands they buy in Asia are doing better than Western brands they try to establish in China.

Where this rise in the consumer buying power in Asia coincides with the question of onshoring of manufacturing jobs in the West is when Asian brands take share from Western brands in Asia, but more particularly when they gain market share in the West. And they will. A few of us are old enough to remember the furious backlash to the rise of Japan in the US during the 1990s. I see the same rhetoric being replayed in the 2000s in regard to China for manufacturing and India for IT services. With the utmost humbleness I submit that by focusing on insourcing/onshoring we are addressing the wrong problem. It may bring short-term relief, and I applaud Obama for closing loopholes that give incentives to companies to offshore, but let’s focus most of our energies on the product innovation that will capture market share in Asia instead. Let’s stop thinking that designing products in the West and selling them in China is the way to go. Let’s learn from how the Japanese established design centers in the US, particularly for cars, and now enjoy the greatest market share in luxury brands. Stalk comments that

Western companies need to understand that Chinese consumers have very different needs than consumers in their home markets. Chinese households don’t want cappuccino machines; they want water filters, air filters, and soy milk makers (at the moment, one of the hotter consumer categories in China—and one with no foreign competition). The classic example involves automakers, which had to learn that many Chinese who can afford cars like to employ drivers—so backseat features are very important to them.

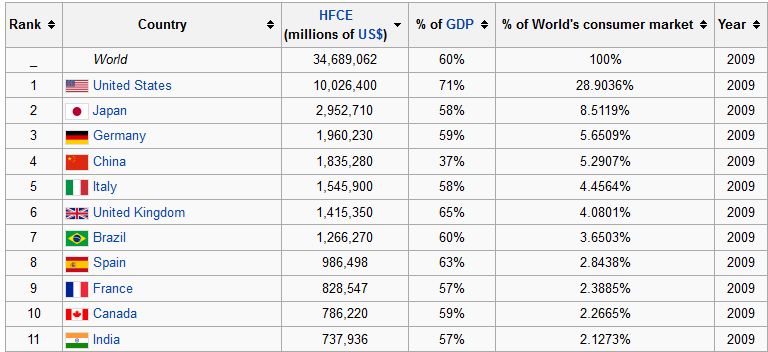

These are all thoughts echoed in a recent book (The USD 10 Trillion Prize: Captivating the Newly Affluent in China and India) published by a number of BCG people. The book is based on a study in which they find that consumers in India and China are expected to spend nearly $10T on goods and services a year by 2020. To put this into perspective, below are the household final consumption expenditure numbers of the top 11 countries in 2009, in which the combined HFCE for China and India was about $2.5T, or a 290% growth over 11 years, averaging out to 26% annually, or 13.1% CAGR.

The authors make two important and related observations or predictions

- We are at a turning point in history where relative wealth will shift from the West to China and India, but absolute wealth, including in the West, should increase.

- It is not a zero-sum game. But Western businesses and individuals wishing to gain share need to act now. They must choose to be contenders, and remake their dreams for a new world in which China and India play a much larger role - but where the West can still prosper. That's the real lesson of The USD 10 Trillion Prize.

I admit that I would hate to be in Detroit in my early 50s with over 30 years of automotive experience and no education beyond high school. So while this is not a zero-sum situation, let us not mortgage the future of our children for the expediency of the present. Structural changes are required, and these are always painful, especially for the people who bear the brunt of the restructuring.

Discussions

Thanks.

Yes, I agree, there is more to it than rising fuel costs. I also referred to inflexible supply chains with long lead times.

I hope that, for example, Western companies will develop a killer soy milk maker.

Regards

Trevor

Increasing marine fuel costs, higher wages in China, and inexpensive natural gas in North America is opening up the world of manufacturing again. Exciting times to still be here and have real manufacturing skills.

Also, an increasingly visible difference between cheap import goods and high quality artisan produced items is leading to more domestically sourced goods.

The Maker Movement and an increased cachet for 'Made in USA' is the third leg driving this.

Union concessions are likely necessary to continue this trend.

Here's a good review of how GE has successfully brought some of there production back to the USA: http://www.producracy.com/domestic-manufacturing-the-insourcing-boom/

-Andrew

Leave a Reply